What retailers need to know about the second round of PPP loans, how to apply for new employee tax credits and other ways to optimize their personal taxes for 2020 and moving into 2021.

Updated 1/18/2021

The PPP has been given new life, meaning certain businesses can apply for a second loan, though the terms have changed. In this next round of funding, the short story is that businesses must have at least a 25 percent drop in revenue in any quarter of 2020, compared to 2019, to be eligible. This means you must have had at least a 25 percent drop in revenue from, for example, April-June (Q2) 2020 when compared to April-June (Q2) of 2019. To be eligible, a business must:

- Have no more than 300 employees with no less than 25 percent reduction in gross receipts in the first, second, or third quarter of 2020 compared to the same quarter in 2019. Applications that are submitted after January 1, 2021 may qualify with a 25 percent reduction in gross receipts in the fourth quarter of 2020 compared to the fourth quarter in 2019.

- Have received and used the full amount of the first PPP loan.

Eligible businesses can apply for a loan that equals 2.5 times their average monthly payroll for the entire year. That said:

- This might be a different number than previously used which was for a shorter average monthly period. Since businesses may use the average monthly billing for the whole year of 2019, the 2.5 times average monthly payroll may be more than asked for in a previous application. This should be an easy calculation to determine, if that is the case, for most businesses.

- Accommodations and food service companies can use 3.5 times their average monthly payroll. This could give restaurants and other hospitality businesses one more month of payroll or other costs to keep them going. Alas, this is not the relief most restaurants are looking for.

- The maximum available loan is now $2 million.

- Forgiveness amounts will be either the lessor of the covered expenses or the payroll costs divided by .6.

- All the guidance from the SBA for the first round of PPP loans will apply to these second-draw loans.

What about added additional eligible expenses? Here they are. These loans:

- May be treated retroactively so you could ask for more money.

- Are not available if your loan has already been forgiven.

- Include operation expenses for software or cloud computer services.

- Include property damage costs due to damage or vandalism from protests/disturbances during 2020 not covered by insurance.

- Supplier costs are covered if they are made to a supplier of goods that are essential and are made pursuant to a contract before the covered period.

- Worker protection expenditures are covered, including acquisition of PPE, and operating or capital expenditures to adapt the business to requirements established by guidelines from Fed, State, or local governments. This does not include residential real property.

Forgiveness applications have been simplified to include a one-page application for loans up to $150,000 and a three-year record-keeping requirement. Payroll costs include everything we thought, but the legislation clarified that group insurance costs are included.

And what about existing PPP loans in excess of $2 million? The necessity doctrine did not disappear for loans of more than $2 million. Be sure to have your attorney review that form before it goes in. The legislation includes new calculations for farmers and ranchers. Farmers and ranchers can apply for a loan that equals the farm gross income divided by 12 times 2.5 (if there are no employees). Schedule F folks may add 2.5 times their employees average monthly payroll.

The covered period is now any period between eight weeks and 24 weeks (instead of eight weeks or 24 weeks). Congress left it vague and has not told us if we had to wait.

Be sure you come up with enough expenses to get total forgiveness.

ERC (Employee Retention Credit)

Okay so this is actually huge — you must have employees to be eligible (If you are an S-Corp and you are on payroll, you are an employee). This credit can get your business up to $5,000 per employee for 2020 in your pocket. Yes. That’s not a small amount. And for 2021 it increases up to $7,000 per employee, per quarter. In order to qualify for this, you must have employees on payroll – freelancers/sole proprietors with no employees are not eligible. For 2020, you must have either:

- At least a 50 percent drop in revenue for any quarter in 2020 compared to 2019, or;

- Been shut down for COVID per a government order.

The rules are different for 2021.

PFL (Paid Family Leave)

The Coronavirus Families First Act (that provides paid leave) was extended from December 31, 2020 through March 31, 2021. This Act can help put money back in your pocket if you or your staff needed to take paid time off due to COVID or had a lack of childcare. All the basics are here. If you’re self-employed (not on payroll) you would claim the credit when you file your taxes. Any time off for your team would be claimed on your 941(s). It might not be too late to claim the credits for 2020, either! Check-in with your payroll provider on backdating the information.

EIDL (Economic Injury Disaster Loan)

If you received an EIDL grant, it no longer will reduce your PPP forgiveness amount. Already filed for forgiveness? Reach out to your lender.

Donations/Gifts Are Not Taxable

WHOA. Hey. Did you get money during 2020 from friends, family, strangers, etc? That income may not be taxable. We know a lot of the gig workers gave and received lots of $$$ during 2020 to support each other. Please make sure you have this flagged properly and are not paying tax on it if you do not need to.

Even if it was paid to your business. Funds received with no consideration (aka, the giver doesn’t want anything from you, you didn’t promise anything in exchange for the money, you didn’t give anything in exchange for the money, etc) – money given out of the kindness in someone’s heart – is not taxable.

ALSO – if you had/have/will have a Kickstarter or other type of crowdfunding – if you aren’t giving anything in exchange for the funds – it’s not taxable.

Updates and explanations courtesy of Rose, Snyder and & Jacobs LLP and Countless.

______________________________________________________________________________

Updated June 6, 2020

PPP Loan Forgiveness & Extensions

- The extension of the time for using loan proceeds, and an increase in the percentage of loan proceeds that can be used for expenses other than payroll.

- The PPP Flexibility Act extends the timeframe (e.g. the covered period) in which PPP funds must be used in order to have the loan forgiven. The 8-week covered period has been expanded to 24 weeks (but ending no later than December 31, 2020).

- 60 percent can now be spent on payroll and 40 percent on other costs versus the original 75 percent on payroll and 25 percent on other costs such as rent, utilities, and interest on mortgages.

- Previously, the exception for not restoring your workforce was if an employee refused to come back to work (make sure it’s documented and reported to UI). We now have the following exceptions:

- Inability to hire similarly qualified employees or;

- You cannot restore operations to comparable levels of business activity due to government restrictions.

- Basically, they’re admitting and understanding that things likely aren’t going to be the same, and exceptions will be made. They know it’s not fair to penalize employers that literally cannot operate in the same manner they were before. This is great news.

5/1/2020

- PayPal – PayPal (owned by eBay) has streamlined the application process. You will literally hear back from them within 24 hours as to the submission of your application. They will email you updates to how it’s moving along.

- Funding Circle – Similar to PayPal’s process. You will get emails at every step of the application process.

- Kabbage – Kabbage’s process operates like eBay’s and Funding Circle. You will literally hear back from them within 24 hours as to the submission of your application. They will email you updates to how it’s moving along.

- Lendio – Same as listed above.

- Fundera – Same as listed above.

Can I and Should I apply for multiple PPP loans?

You can apply for multiple loans, but you can only accept a loan from one bank. The problem with this is that too many applications will trigger fraud flags and could cause delays in your application.

In general, it may be best to apply for one loan with your financial institution. You may also want to try ONE source from the list above. Gary strongly cautioned against making too many applications for PPP loans.

Already approved PPP applications are starting to be funded. According to COVID Loan Tracker:

- The PPP loan disbursement rate (people who actually received money) is low but climbing: 9.52%

- The number of businesses “approved” by the SBA for PPP is increasing: 29.9%

- Median loan size: $80,250

- Median processing time: 9 days (this should speed up for the second round as applications are already saved).

How Do You Make Money While You Navigate Insurance, Loans, and Grants?

04/26/2020

Last week, the Senate passed an additional $320 billion in funding for small business PPP loans and another $60 billion in disaster loans. The bill went to to the House, where it passed. New funding starts today.

As you many retailers know, the PPP loan process has been nothing short of a nightmare. As loans were announced and amounts disclosed, small businesses and brands began to protest and petition the prioritization of the loan amount over the requirement of first come, first served. Because of this:

- Roughly 80% of U.S. small businesses have been unable to get PPP loans (that’s millions of people).

- Small businesses are suing four major banks, including Wells Fargo and Bank of America, alleging they accepted applications based upon the loan size rather than on a first-come-first-serve basis, as required.

- Larger companies are coming under attack for receiving funding, including Shake Shack, which said it is returning the $10 million of PPP loans it received.

- Publicly traded companies received $300 million worth of PPP loans, and small businesses want them to give it back so that smaller companies have a chance at surviving.

- Many say an additional $320 billion still isn’t enough.

What that means for you as a small retailer:

- If you started an application for a PPP loan, call your bank and see where it’s at. The additional funding would allow them to reactivate your submission.

- If you haven’t applied, apply, but only submit one application at a time.

- If you need help with the application and funding process, look at Fundera and Kabbage as they are creating a central referral to bank funding service to help small businesses.

- Continue to look for grants from other organizations and state-level resources.

- If you receive a loan, listen to this webinar about making sure you get the forgiveness that comes with it.

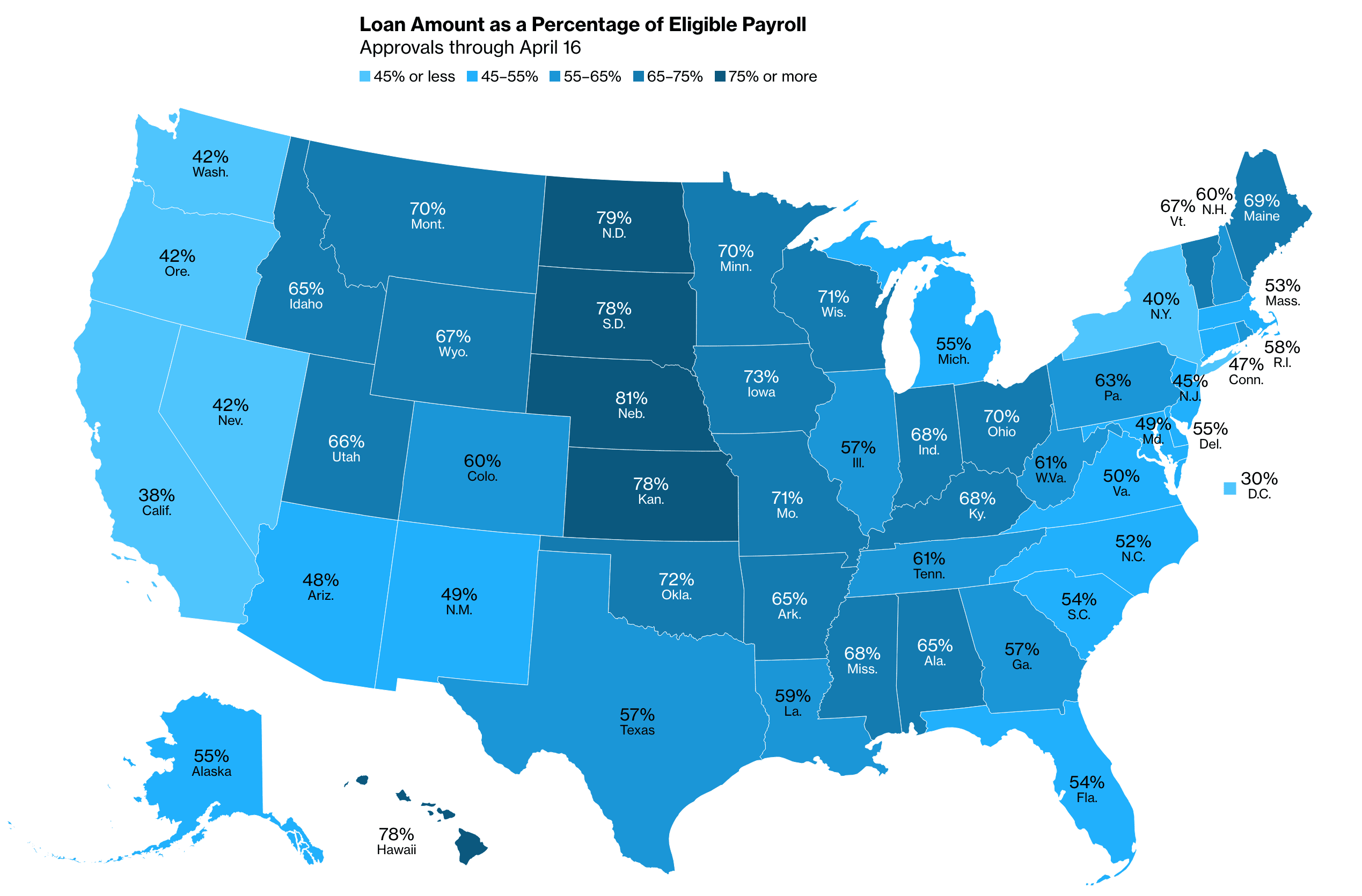

Loan Approvals Percentages By State

04/20/2020 – PPP Loans and Small Business Updates

As of last week, the Small Business Administration (SBA) announced that it had committed $349 billion in funding for the Paycheck Protection Program (PPP). The SBA reported that 5,000 lenders have approved 1.6 million loans totaling $342.2 billion. “The SBA has processed more than 14 years’ worth of loans in less than 14 days,” according to a joint statement from U.S. Treasury Secretary Steven T. Mnuchin and SBA administrator Jovita Carranza.

The problem is most of the loan funds didn’t go to small businesses, they went to mid-size chains like Ruth Chris Steakhouses, Potbelly Sandwich Shops and several energy companies who received millions in SBA PPP funding. There’s been a tremendous backlash as small businesses (those will less than 15 employees) have to close their doors because their requests for smaller loan amounts went largely overlooked.

According to COVID Loan Tracker, businesses that were classified as “small” that have managed to secure funding had an average of 15 employees and received an average of $120,000. Once the disbelief and confusion have run their course, small business owners and small retail store owners will shift gears and figure out what to do (whether they received funds or not). Sadly, many retailers are reporting that they will have to close their businesses.

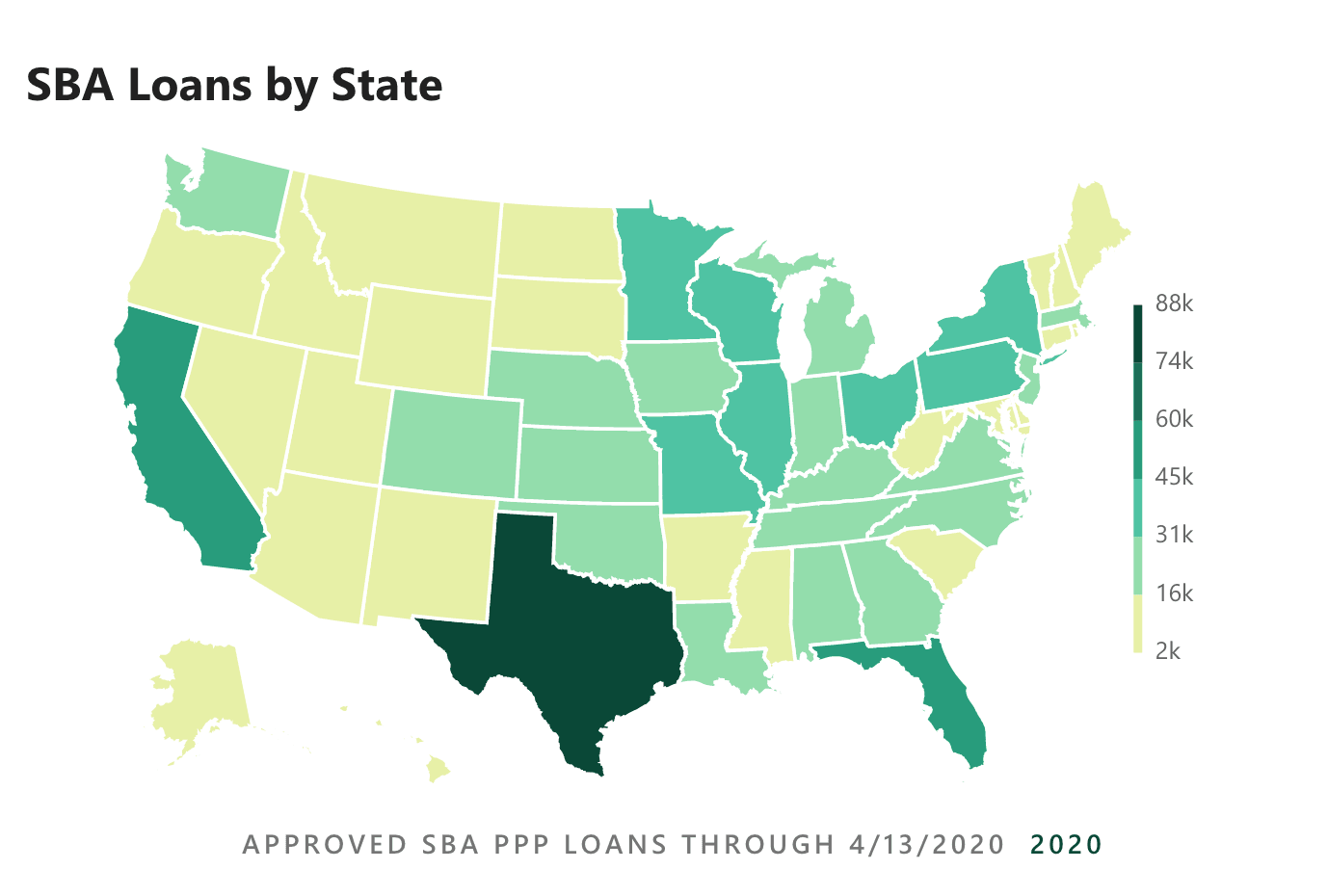

Where The Funds Went: By State, Industry and Loan Amount

Most banks (those on this list) are saying that they hope additional funding will be approved by Congress, so they can keep processing the loan applications. If you’ve already submitted a loan application, most banks are holding these for up to 30 days in the event that additional SBA funding becomes available under the same terms and conditions. Understand that there is no guarantee that additional funding will become available or that it will have the same terms and conditions.

What Can You Do Now

Small business owners are still encouraged to check for resources at the state level and to seek grants; most of these programs (like ones in New York) have been depleted. If you live in a heavily impacted area, the U.S. Chamber of Commerce just launched $5,000 small business grants. Apply today as these will go fast.

Updated 4/20/2020: There could be further congressional action on Tuesday or Wednesday to enable banks to open back up the funding for the PPP loans, which could offer further relief. So contact your lender if this happens!

If you’re a medium to large retailer, you truly need funds and are willing to take out a $1 Million dollar loan, the Federal Reserve’s new Main Street Lending Program could be your next step for hope. The program, which is now open to companies with as many as 10,000 employees and will be run directly through lenders, will support up to $600 billion in new loans (read the fine print).

You can also Contact your Representative and Contact your Senator to advocate for more funds to be allocated to small businesses. You can also submit a Freedom Of Information Act for information and records from the SBA. Legally they have to respond in a certain timeframe.

04/03/2020

As of today, you can start to apply for the SBA 7(a) loans, also known as the Paycheck Protection Program (PPP). This is a separate program from the SBA disaster loans (EIDL). In order to apply for these loans, you’ll have to apply through an approved SBA 7(a) lender or federally insured depository institution or credit union.

Here are some things to note:

- You Have To Apply For The Loan: Read this article on How to Obtain an SBA Coronavirus PPP Loan and Have It Forgiven.

- Apply Early: Funds are limited for these loans, while banks have access to $349 billion, financial analysts suspect it’s going to run out fast.

- Have Your Documents In Order: You’ll need your 2019 taxes (including Form 941 Quarterly reports), payroll information and related payroll registers/details for the prior 4 quarters. Have your loan application ready.

- Contact Your Current Bank: Some banks are only offering loans to pre-existing customers. Others are prioritizing their current customers. Contact your local branch/bank to see if they are part of the SBA 7(a) loan program. If not, seek out another bank.

- Make Sure You Educate Yourself: While the loan process might seem easy, it’s not. Funds are going to take at least 30 days to hit your bank account (some financial experts say longer). Do your research when applying for the loans. Make sure the lender is on the approved list and check the interest rate (which is .05% – 1%). Zoe Financial has a webinar April 8th, 2020 specifically designed to educate you on the CARES Act and PPP.

Below is the list of some of the SBA’s most active lenders (there are over 1800 approved lenders), along with links where you can apply. Remember, this is not a full list as smaller, more regional financial institutions are in the process of rolling out their ability to process loans for their customers.

- 21st Century Bank

- America First FCU – Apply at this link by clicking “Apply Now”. You’ll need a business account first.

- Ameris Bank – Fill out an application here and submit to PPP@amerisbank.com. See more details here.

- Atlantic Capital Bank

- Bank of America – A guide is posted here, you must have been a customer as of 2/15/2020.

- Bank of George – See documents you’ll need here.

- Bank of Hope – Call 888-972-5363 for details.

- Bank of the West

- BankUnited – Begin collecting documentation now, including Form 941 from the most recent four quarters and verification of payroll cost and employees for the last 12 months. See updates here.

- BBVA Compass – You can apply here. See other options here.

- Berkshire Bank – They suggest filling out a Contact Us form because of high call volume.

- Byline Bank – Updates will be here. If you’re a current customer, contact your Portfolio Manager.

- Cadence Bank – Learn more.

- Capital One – Application posted here.

- Cathay Bank

- Celtic Bank – You can apply here.

- CenterState Bank – Complete a form here.

- Centerstone SBA Lending, Inc.

- Chase Bank – apply here.

- Citizens Bank – Updates will be posted here.

- Comerica Bank – Call 888-444-9876. Updates will be posted here.

- Customers Bank – Complete the form at the bottom of the webpage for updates.

- East West Bank – Fill out the inquiry form here.

- Embassy National Bank

- Falcon National Bank – Phone numbers and emails to contact are listed here.

- Fifth Third Bank – You’ll need an online banking profile first and you can only apply online. See more details here.

- FinWise Bank

- FirstBank – Download an application here and then email it to your FirstBank banker.

- First Chatham Bank

- First Commonwealth Bank – Complete an application here and include 2019 Form 941 or Form 944 and a beneficial ownership form. Upload the application on their DropBox site or mail the application. See more details here.

- First General Bank

- First Home Bank – Start applying here.

- First-Citizens Bank & Trust Company

- First IC Bank

- First Financial Bank – Details will be posted here and First’s SBA clients will also get emails.

- First Horizon Bank – Update here and contact your banker for more details.

- First National Bank of Pennsylvania – Updates here.

- First Savings Bank – If you’re a current banking customer, contact one of their lenders or call 1-833-372-4968.

- First United Bank – Apply here.

- First Western – Updates will be posted here.

- Five Star Bank – Contact your relationship manager for details, or see phone numbers near the bottom of the page here.

- Fountainhead SBF LLC – Fill out an application here to be entered into the processing queue. You’ll get a welcome email with details on more steps to take.

- Frost Bank – Plan ahead by gathering all the required documentation and then talk to your banker. More details are here.

- Fulton Bank – Applications will be accepted starting April 3. Download an application here, save it and email it to PPPSB@fultonbank.com. See details here.

- Hana Small Business Lending, Inc.

- Hanmi Bank – Details here.

- Harvest Small Business Finance, LLC

- HomeTrust Bank – Updates will be here.

- Huntington National Bank – See their PPP page here. They list what documentation you’ll need along with other relief programs.

- IncredibleBank – See details here.

- Independent Bank

- KeyBank National Association – Fill out a form here for updates.

- JPMorgan Chase Bank – They aren’t currently accepting applications but will post updates here.

- Live Oak Banking – Sign up here to see when they’re accepting applications.

- M&T Bank – Updates may be posted here. They also have an SBA loan page, but it isn’t updated yet with CARES information.

- Metro City Bank

- Midwest BankCentre – PPP fact sheet and details are here. Call 314-631-550 or 800-894-1350 with questions.

- Midwest Regional Bank – A page here simply says not to email personal or financial information.

- Mountain Pacific Bank – Contact your loan officer at 425-263-3500 or wait for updates here.

- MUFG Union Bank

- NewBank

- Newtek Small Business Finance, Inc.

- Northwest Bank – Updates here.

- Old National Bank – Applications open April 3. Contact a loan officer for details.

- Open Bank

- Patriot Bank

- Pacific Western Bank – Learn more here.

- Peapack-Gladstone Bank – On this update, the bank says to email PGBCovid19PPPRelief@pgbank.com for help.

- Peoples Bank of Alabama – Complete a form here to be contacted.

- Pinnacle Bank – Talk to your Pinnacle financial adviser or find one here.

- PNC Bank – Click “Contact Us” for details.

- Poppy Bank

- Quantum National Bank – Applications will be posted here.

- Readycap Lending, LLC – Start the process here.

- Regions Bank – Updates here.

- Republic Bank – This page briefly mentions PPP along with other options.

- Royal Business Bank

- Seacoast Commerce Bank – Scroll down to the Protection Loan section near the end of the site and click on “Apply Here.”

- Seacoast National Bank

- Shinhan Bank America

- Stearns Bank National Association – PPP loan applications won’t be accepted until April 10.

- Stone Bank

- Sunflower Bank – Get updates here.

- Synovus Bank – You can apply online on April 3. Be notified here.

- TCF National Bank

- TD Bank

- The MINT National Bank

- Truist Bank d/b/a Branch Banking & Trust Co – Trustmark has a page about applying here.

- Umpqua Bank – Visit here for all relief options. Sign up here for PPP updates.

- UniBank

- Union Bank – Updates are posted here.

- United Business Bank

- United Community Bank – Sign up here for updates on PPP.

- United Midwest Savings Bank

- Univest – They’ll begin accepting loan applications on April 3 and April 10. Complete an online application here and send it to PPP@univest.net.

- U.S. Bank, National Association – Updates will be posted here.

- US Metro Bank

- VelocitySBA – Not yet accepting applications. Check here for updates.

- Wallis Bank

- Wells Fargo Bank – You’ll be able to apply online here.

- West Town Bank & Trust – Complete a contact form here for a pre-application. Get more details here.

- Zions Bank – An application will be here.

If you’re rejected for this loan, there are still many other options available. Your state might be offering loans for small businesses. You might also be able to apply for a disaster assistance loan through the SBA. The SBA is also offering Enhanced Debt Relief. Almost all banks have traditional small business loans available; these loans carry 5–10 year repayment options at interest rates of 4–7 percent.

Also, be advised that there’s already talk of Congress extending the 2.5 month loan provision should the economic impact of the Coronavirus extend beyond that. That would mean that the loan would also be extended IF THIS IS NEEDED.

During this time, we’re here to help you. Find free resources on COVID-19 on our resource page or join the conversation on Facebook. You can also read articles on our blog for free.

0 Comments